Why Mr DIY could be a Worthy Investment Opportunity — Outlook for the Incoming IPO (Part 2)

Disclaimer: I bear no responsibility to any actions or decisions taken by anyone pertaining to this research.

I previously wrote about Mr DIY in Part 1 here, and how Malaysia is looking like for a company selling various household goods and items. Since then, Mr DIY’s prospectus has been released here. I will be taking a close look at its financials and hopefully decide whether RM1.60 is a fair value for Mr DIY. To recap, Mr DIY will be listing its shares to the public possibly by the 4th quarter of 2020, hoping to raise about RM1.5bn with a price of RM1.60 per share.

Mr DIY has bullish revenue growth and is expected to grow even more

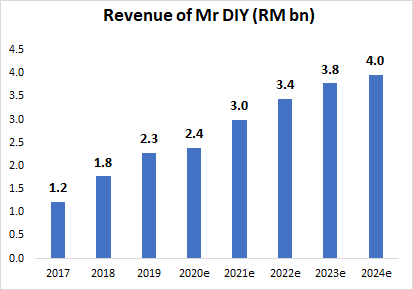

Revenue grew strongly by 44.1% and 28.5% in 2018 and 2019 respectively, generating a revenue of RM2.3bn. While the 1st half of 2020 was hit hard by the movement control restrictions, Mr DIY managed to grow its revenue by 4.4%, defying the overall expectations of a decline. This was due to households having more time for home improvement activities and that sustained the sales of Mr DIY during the MCO period.

Mr DIY is aiming to continue its aggressive expansion plan by opening 200 stores in 2020 and 2021. It currently has 636 stores in Malaysia as of 30 June 2020, with another 153 stores to go to reach its 200 stores target by end-2021. Mr DIY is expected to generate more revenue with its aggressive expansion to capture market share. Currently, its 632 stores constitute about 8.8% of all home improvement retail stores, making it one of the biggest player. With its additional 200 stores target by 2021, its market share is expected to grow to 10.7% of all retail stores.

Mr DIY has been consistently profitable, while being efficient at doing so

Mr DIY’s profit margins are considered healthy, averaging 15.2% from 2017 to 2020. Profit margins did decline in 1st half of 2019, but recovered towards the end of 2019. Considering that the MCO hit in the 1st half of 2020, Mr DIY’s margins did hold up quite well.

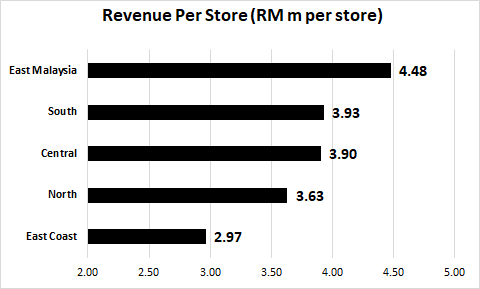

Mr DIY’s revenue are driven mainly by Klang Valley and the Southern states, but its most profitable region is surprisingly East Malaysia

About one third of Mr DIY’s revenue comes from the states of Kuala Lumpur, Selangor, and Putrajaya, generating close to RM718m in 2019. The southern states of Negeri Sembilan, Malacca, and Johor generate about 21% of revenue, followed by Sabah and Sarawak (17%), Northern states (16%) and the East Peninsular Coast (13%). Mr DIY has been more aggressive expanding in the Klang Valley, with the amount of stores almost doubling from 101 stores in 2017 to 184 stores in 2019.

However, Mr DIY stores in Klang Valley are not the most profitable. That title belongs to Sabah and Sarawak’s stores. Revenue per store in East Malaysia was the highest at RM4.5m per store, followed by Southern States (RM3.9m per store) and Klang Valley (RM3.9million). It is probably the case that competition is much tougher in Peninsular Malaysia compared to East Malaysia. While most of Mr DIY’s revenue is derived from Peninsular Malaysia still, I think its worth it to venture more into East Malaysia as we have typically neglected the market there.

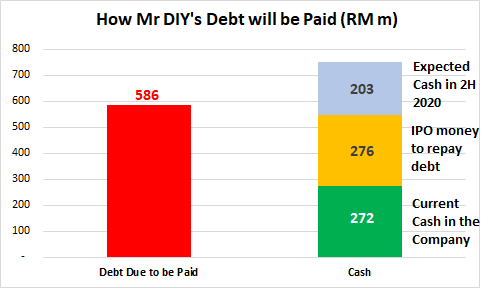

Debt increased considerably in 2019 to fuel its store expansion, but should not be a concern

Mr DIY’s total debt increased by 20x from RM31m in 2017 to RM623m in 2019, where it drew down on RM600m worth of debt in 2019 to fuel its aggressive expansion. It has about RM586m worth of debt that is due in 2020, which is massive considering that it has only RM272m in cash.

The only reason this is not worrying is because it intends to use RM276m from its IPO to repay its bank borrowings. This amounts to a total of RM548m, where the difference could be made up from its healthy operating cash flows. Mr DIY is on track to generate at least RM400m in cash from its operations, considering that it has generated RM200m in the 1st half of 2020.

Mr DIY’s RM1.60 per share is fairly priced, considering its future prospects

Mr DIY’s issuance of RM1.60 per share is fairly priced in my opinion, at a price earnings ratio of 31.6 times. I ran the numbers through my financial valuation here, and concluded that the current issue price is fair. What I mean by fair here is that I think it makes sense for Mr DIY to trade at this price. It is by no means undervalued or overvalued.

I arrive at this valuation by projecting a revenue growth of 5% for 2020 and 25% for 2021, and EBITDA margin of 30.0% consistent with historical data. I do think this valuation is fair as Mr DIY is expected to have 785 stores by 2021. With an assumption of RM3.8m per store (2019), Mr DIY is expected to generate about RM3.0bn in 2021, which is consistent with the growth rates I have assumed for 2020 and 2021.

Conclusion

In conclusion, RM1.60 for Mr DIY seems fair. Considering its aggressive expansion plans to build new stores, Mr DIY is poised to capture more of the home improvement market in the future and could amass about 10% of the market in Malaysia. Its financials are solid, and it doesn’t have any glaring faults.